Since the mortgage brokers’ business model is based on one-time fees, your business depends heavily on the constant acquisition of the best mortgage leads.

Developing one or more streams of inbound leads is key in this industry, and mortgage brokers must familiarize themselves with a few marketing strategies to survive.

The U.S. mortgage/loan brokers market is projected to grow at a compound annual growth rate (CAGR) of over 5% from 2024 to 2029 (source: Modor Intelligence). So there is no better time to learn how to get leads as a loan officer.

In this article, I will first review the different types of mortgage leads you can generate, then I will share the smartest ways to find mortgage buying prospects, and finally, I will share how I transform my leads into customers.

The different types of mortgage leads

Mortgage refinance leads

Although these prospects have already closed a mortgage, there always comes a time when they are back into the mortgage market: mortgage refinancing.

You can increase your chance to contact a lead when he is warm for mortgage refinancing by following these indicators:

| Indicator | Broker’s strategy |

| Interest rates are low or drop | Keep an eye on current mortgage interest rates. If rates drop significantly, it may prompt homeowners to consider refinancing to lock in a lower rate. Set up alerts for rate changes or send out emails/notifications to customers when rates fall, informing them of potential savings through refinancing. |

| They’ve built significant equity | A homeowner with 20% or more equity in their home is more likely to be eligible for favorable refinance terms. This could be due to rising home values or paying down the mortgage principal. If a customer has gained equity in their home, they may be ready to refinance to access cash for renovations, debt consolidation, or other financial goals. The easiest way to know this information is to track all your customers in a CRM, and set up a reminder after a few years, when the equity has increased. That’s a very long term stragegy. If you want faster results, you can also educate your current customers about this opportunity via social media and emailing. |

| Improved credit score | If a customer’s credit score has improved since they originally took out the mortgage, they may now qualify for better refinancing terms. This can lower their interest rate and overall loan cost. Encourage customers to check their credit reports regularly and reach out when their scores increase to a level that may lead to refinancing eligibility. |

| Changes in financial circumstances | Debt Consolidation: Customers experiencing debt problems (e.g., high-interest credit card debt) may consider refinancing to consolidate their debts at a lower interest rate. Income Increase: If a customer’s income has increased, they may be in a better financial position to refinance and take advantage of better terms or faster repayment options. Life Events: Events like marriage, divorce, or having children may change a customer’s financial situation, making refinancing more attractive for adjusting their loan terms. To take advantage of these changes, you either have to know your client intimately, or make them aware of the advantages (via social media or emailing) before the event occurs, so that when the timing is right, they know they can approach you. |

| Desire to lower monthly payments | Refinance for Lower Payments: Customers may want to refinance to reduce their monthly mortgage payment, especially if they are struggling financially or want to free up money for other expenses. Loan Term Adjustment: Switching to a longer loan term (e.g., from 15 years to 30 years) can reduce the monthly payment, making it more manageable. Push the information to your current customers via email. |

Aged mortgage leads

These are the leads that have shown interest in receiving a quote for their mortgage a long time ago. They have probably received quotes from other mortgage brokers, but may still be in-market for a mortgage.

Aged mortgage lead cost is lower (around 1$ per lead) due to their age (30-85 days old). Their conversion rate is also usually lower, due to the numerous quotes that have already received.

Closing aged mortgage leads is therefore a volume game. A good marketing strategy is to buy them in bulk, and run an email sequence with the objective to get a call from the few still interested in receiving a quote.

Live transfer mortgage leads

If you want the freshest leads, live transfer is what you need.

Here is how it works:

- A mortgage lead generation agency takes care of generating calls from leads interested in receiving a quote for their mortgage

- As the leads call the line, the agency transfer them to your direct line

- You conduct the call

The advantages of live transfer for mortgage leads are:

- Controlled ROI: You pay only when you have a lead on the phone

- Time efficiency: You don’t spend time generating leads

On the other hand, live transfer mortgage leads are more expensive. You need to work on your sales pitch to optimize your phone-to-client conversion rate in order to make this channel profitable.

Reverse mortgage lead

Reverse mortgage is a type of loan available to homeowners aged 62 or older, allowing them to convert part of the equity in their home into cash.

Timing is key to capture reverse mortgage leads, and a mortgage broker needs be familiar with the indicators that increase chances for a homeowner to be in-market for a reverse mortgage.

| Indicators a Lead is in-Market for a Reverse Mortgage | How to Capitalize on These Indicators |

| Age and Life Stage: Homeowners aged 62+ or those in retirement planning. | Track the age of your customers in your CRM, and set a reminder when they hit 62 years old. |

| Customers experiencing financial difficulties, credit card debt, or rising healthcare costs. | Offer personalized advice, clarify questions, and schedule a consultation. |

| Life Events: Health issues, recent retirement, or desire to downsize. | Know your customers. When the time is right, gently step in with a tailored offer. |

How to get mortgage leads

Mortgage credit trigger leads

In the mortage industry, timing is key. And a credit trigger is the sweet spot for you to show up.

Mortgage credit trigger leads occur when an individual applies for a mortgage loan and a hard credit inquiry is made by the lender. A hard inquiry is when a lender checks a person’s credit report to evaluate their creditworthiness. Once this inquiry is made, the credit bureaus share this information with other lenders as part of a marketing product. These lenders can then use this data to send competitive offers to the individual.

As soon as the credit report is pulled, other companies can start reaching out to the applicant with offers, sometimes within a very short time. You must act quickly during this “sweet spot” to present your offer before other mortgage brokers do, or before the individual decides to opt-out of receiving offers.

How to transform mortgage credit trigger leads into customers:

- Collaborate with services that offer credit trigger lead data: These companies can notify you when a person has had a recent hard inquiry, enabling you to send targeted offers quickly.

- Speed is critical: Ensure that you are able to respond quickly to a potential lead (we are talking about seconds here). The faster you act, the higher the chance of converting the lead before competitors do. Consider automating responses or setting up alerts to act immediately when a trigger occurs.

Buying mortgage leads

If you want immediate results, buying mortgage leads for sale is a good option. However, all the leads are not equal, and you need to consider two main factors:

- The Cost Per Lead (CPL)

- The lead quality

CPL: Good quality leads have a high CPL and low quality leads have a low CPL.

Lead Quality: You need to review the quality of the leads before buying them. This can be complicated since not all mortgage lead agencies are sharing these information with you. And even if they do, you sometimes have no way to verify this information and rely on their good faith.

Here are some factors that impact the lead quality:

Lead Age: when was the lead generated: 5 minutes ago? 5 days ago? 5 weeks ago? The lead age influences greatly its quality as it may have been in contact with several other mortgage brokers in the meantime

Exclusive vs. shared leads: Are the leads sold exclusively to you? Or are they sold to multiple mortgage brokers? By buying exclusive mortgage leads, you have the advantage to be the only broker contacting them, reducing competition as a result. However, exclusive mortgage leads are more expensive than shared leads. If your offer is competitive, it might be more profitable to buy shared leads, as they will cost you less, and you will have an edge to your competitor with a strong, competitive offer. Choose the strategy that works best for you.

Qualified leads: this defines what filters have been applied to the leads before being sold to you. This usually boils down to what qualifying questions were asked to the leads. Example: what’s your equity on the house? What’s the value of your house? Etc. As a mortgage lead buyer, you can select the leads that fall under specific groups, increasing your return on investment as a result.

Their ease of use, guaranteed leads, and focus on local reach make them an excellent choice for businesses looking to grow their client base effectively.

Generate local mortgage leads with Google Business Profile

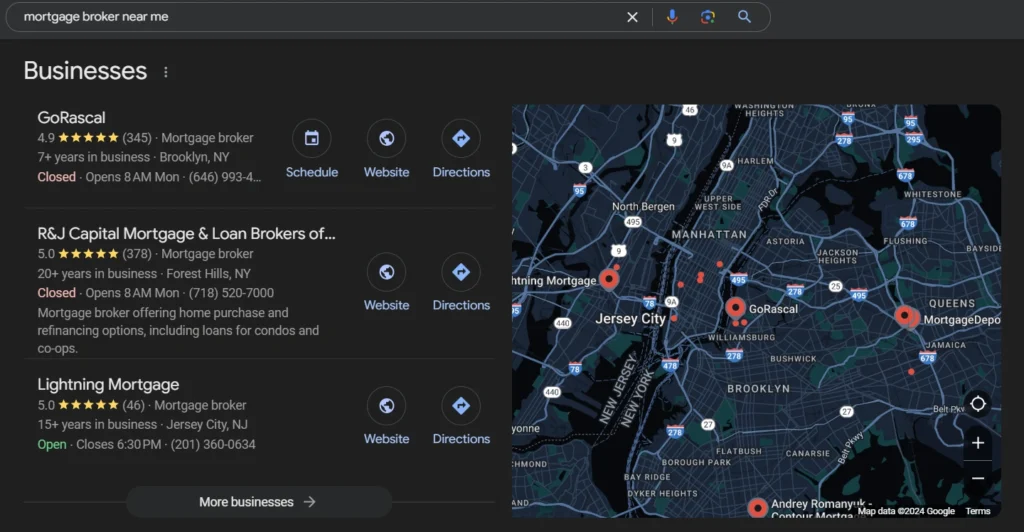

Google Business Profiles appear organically on Google’s Local Pack for local queries, such as “Mortgage broker near me”, allowing you to generate local mortgage leads.

You simply need to create a Google Business Profile. When someone around you searches for your services, you appear in the Local Pack (see image). Users can engage with your business either by calling, texting, visiting your website, leaving a review, or asking a question.

To increase your organic ranking of your Google Business Profile in the local pack, I advise doing the following:

Step1: Keyword selection

Select the keywords you want to rank for. Write them on Google, check the keyword recommendation at the end of the page, add these keywords in your target list.

Step 2: Create your Google Business Profile

Head to Google Business to create your account. It’s important to setup your account properly as it will impact your ranking in the local pack later. The factors that impact your ranking are:

- The name of your Google Business Profile: Try to integrate your main keyword in the name of your profile. Examples: John Wick Mortgage Broker New York

- The description: Introduce your services. Here, you want to integrate all the keywords you listed before

- The categories: add as many categories as possible, as long as they are relevant for your business

Step 3: List your business details in online directories

Identify both general and industry-specific online directories, and list your business there by adding your NAP:

- Name

- Address

- Phone number

This will tell Google that your business is legit, and will impact your ranking on the local pack.

Step 4: Get positive reviews

Positive reviews is the most important ranking factor. You want to receive regular positive reviews to impact your ranking. One trick that always works is to simply ask your customers to leave a honest review of their experience with your business, so that other people in their situation can benefit from your services.

Make sure to answer to the positive reviews, and manage the negative ones by solving the problem offline, and asking the customer to remove it once the issue is resolved.

Build strategic partnerships

Partner with professionals like real estate agents and accountants to acquire mortgage leads. They know when the timing is right for you to approach their customers. Moreover, when they refer you to their customer, they pass you the trust they have built with them, providing mortgage leads that are ready to be closed.

Having done a fair amount of strategic partnership in my career, I can tell you that the biggest predicator of a successful partnership is how aligned you are with the vision. Because it takes time and adjustments for a partnership to provide value for both parties, it’s only through a shared vision that your partnership will hold in the first few months. Partners who are only interested in instant money won’t be a good fit, because they will loose their motivation after the first few leads don’t convert.

Become a local star

Be known in your community as a local business owner. Become the local star of your community. So whenever someone needs a mortgage, you will be the first person that come to their mind. You will also be the first referred to those asking for a mortgage broker.

So how to become the local star? Be visible!

- Sponsor your local football team

- Continuously run ads on Facebook and Instagram within a 5-10 miles radius

- Attend local business meetings (organized by associations or your council)

LinkedIn is the best professional network with 310 million monthly active users. Chances are 75%+ of your ICP (ideal customer profile) is on LinkedIn.

How to reach them?

Connect with your ICP: Use LinkedIn search features to identify your ICP and add them as connection. You can currently add up to 200 connections per week, and approval rate fluctuates between 20 and 40%, allowing you to connect with 160 to 320 potential customers each month for free. For more advanced search features, use LinkedIn Sales Navigator (paid feature).

Activate your connections: Post regularly. The goal is to see who “raise their hand” by checking who liked or commented on your post. You can then continue the conversation by messaging them directly.

Familiarize yourself with the post format on LinkedIn by following mortgage brokers with a big following base. Identify the posts that work for them, and replicate them: keep the same hook, and adapt the rest of the content to your own sauce.

How to close mortgage leads

You have now generating a stream of mortgage leads. The most difficult is done!

Now, all you need to do is to transform these leads into paid customers.

Remember, all leads aren’t equal. Some are more ready (more warm) than others (more cold) to close a deal with you. Your job is to warm up your leads, and it takes two things:

- Recurring targeted communication: reaching out to your leads at the right frequency with the content they want to consume

- Time: keep in mind that the lead-to-customer conversion time can take months. It’s not because a client ghosts you today, that he won’t close a deal with you in 6, 9, 12 months from now.

Here are a few strategies to close your leads:

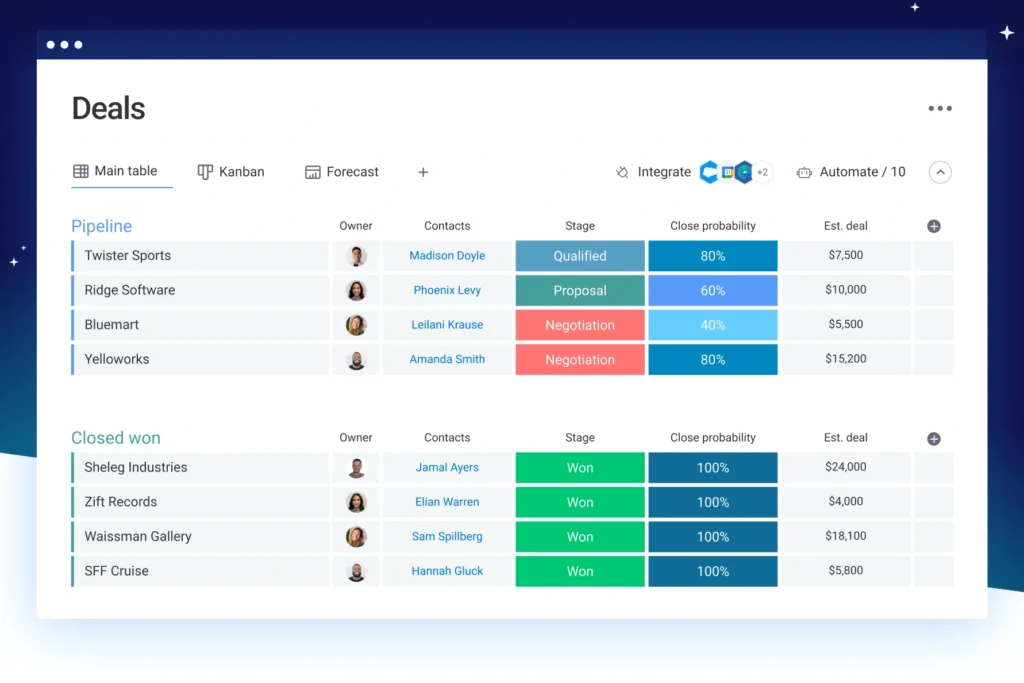

Use a CRM

A CRM (Customer Management System) allows you to build a structured list of leads segmented by sales stage. So you know for each lead what you need to do next to move them down your sales funnel. Popular CRM include Monday.com and Pipedrive.

Use your CRM to extract valuable data such as the lead-to-customer conversion rate for each marketing channel, or the CPO (Cost per Opportunity) and CPA (Cost per Acquisition aka. Cost Per Sale) to understand which channel provides the best leads.

Although mortgage lead conversion rates is estimated to be around 2-6%, there are no right and wrong rates. You can have a 0.25% conversion rate on your mortgage leads, and still kill it thanks to the huge volume of mortgage leads you generate monthly.

Track the source of your leads

You have generated mortgage leads from various marketing channels and ads. And when a lead transforms into a customer, you are not able to link this customer to the marketing channel or ad that generated it. As a result, you don’t know which channel or ad generates business, and keep spending your marketing budget on ads that don’t perform.

Leadsources closes this analytics gap by tracking the source of each lead. So you know which sources bring the most revenue. As a result, you can optimize your marketing channels and ads accordingly by investing more in the channels that bring revenue, and canceling the channels that don’t contribute to your bottom line.

Try leadsources today for free!

Emailing

Send email sequence to your leads. The key here is to send the right message at the right time.

Example of good timing: When rates drop significantly, it prompts homeowners to consider refinancing to lock in a lower rate. Send out the following email to your leads when rates drop:

Subject Line: Are you missing out on today’s low rates?

Body:

Hi [First Name],

Did you know that mortgage rates have changed recently? This could be the perfect time to:

- Lower your monthly payments.

- Pay off your mortgage faster.

- Free up funds for other financial goals.

Feel free to reply to this email if you’d like a personalized assessment of your options!

Best regards,

[Your Name]

Other triggers include:

- Homeowners who have built significant equity and are in-market for refinancing their mortgage

- Improved credit score: send an email to encourage your customers to check their credit reports regularly and reach out when their scores increase to a level that may lead to refinancing eligibility

- Changes in financial circumstances such as income Increase: If a customer’s income has increased, they may be in a better financial position to refinance and take advantage of better terms or faster repayment options.

As you can see, you can only know when the timing is right by knowing your customers. Use a CRM to collect valuable information about them, and use emailing wisely to get them raise their hands.

And like everything, it takes time. Try, improve, and you will generate and close mortgage leads, providing financial gains for you and your family.